– Bridging the Gap in Global Financial statement Analysis

International Financial Reporting Standards (IFRS) are a set of Accounting Standards that govern how particular types of transactions and events should be reported in Financial Statements. They were developed and maintained by the International Accounting Standards Board (IASB). IFRS are now used by more than 100 countries, including the European Union and by more than two-thirds of the G20.

IFRS 18 (Presentation and disclosure in Financial Statements) is the most significant change to the Income statement, which replaces the old IAS 1. It introduces mandatory subtotals like “Operating profit” to make income statements more comparable across companies.

- Restatement Requirement : Companies must restate their 2026 comparative figures to match the new IFRS 18 format when they first report in 2027.

- Key changes : It replaces IAS 1 and introduces a mandatory structure for the Income statement with three new categories :- Operating, Investing and Financing.

- New Subtotals : Operating Profit is now a mandatory subtotal, removing previous flexibility where companies could define this figure themselves.

- Lack of Defined Subtotals : Under IAS 1, there was no official definition for Operating profit. Companies could define it however they liked, leading to “wild freestyle” formats where two similar firms looked completely different on paper.

- Non GAAP chaos : Many companies used “Management Defined performance measures” like EBITDA – outside their official Financial statements without clear reconciliations.

- Limited Guidance : IAS 1 had limited guidance on aggregation, allowing companies to hide important expenses under vague labels like other.

IFRS 18 responds to market demand for greater comparability and transparency with a focus on information about financial performance in the statement of profit or loss. And all companies that apply IFRS around the world will be expected to use the new standard beginning in 2027.

IFRS 18 introduces three sets of new requirements, comprising:

- Two new subtotals in the statement of profit or loss

- Disclosures about Management-defined performance measures (MPMs); and

- Enhanced guidance on the grouping of information in the financial statements.

- The “Spirit” of the Standards

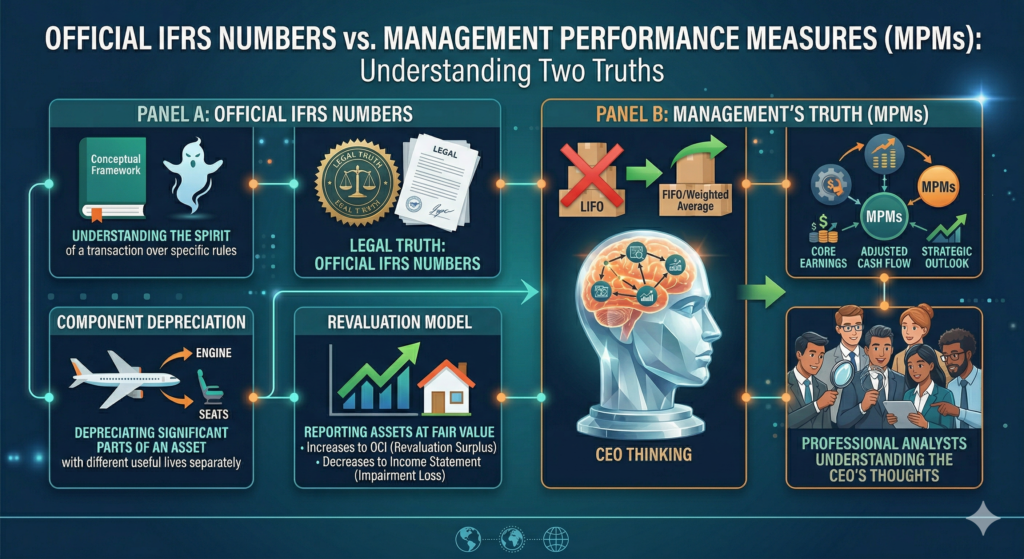

- Principles Based : IFRS is based on a conceptual framework. Understanding the spirit of a transaction is better rather than looking for a specific rule

- Professional Judgement : IFRS allows more management discretion, which means an analyst must check the “Notes to the Financial statements” to understand which assumptions were used.

- LIFO is prohibited : LIFO liquidations can inflate profits unsustainably by using old inventory costs with current revenue. Companies only use FIFO or Weighted Average cost.

- Measurement : Reported at the Lower of cost or Net Realizable Value (NRV). NRV = Estimated Selling Prize – Estimated completion / Selling costs.

- Component Depreciation : You must depreciate significant parts of an asset separately if they have different useful lives (Eg : An Airplane’s Engine v/s its seats).

- Revaluation Model : Unlike the cost model, IFRS allows you to report assets at Fair value.

- Increases goes to OCI (Other Comprehensive Income) as a Revaluation surplus.

- Decreases goes to the Income statement as an Impairment Loss.

- Development costs : These costs are capitalized once “Technical feasibility” is proven. This results in higher assets and higher current year net income compared to U.S GAAP.

- Lessee View : No more “Operating vs Finance” distinction for lessees. All leases (with minor exceptions) are recorded as financial leases.

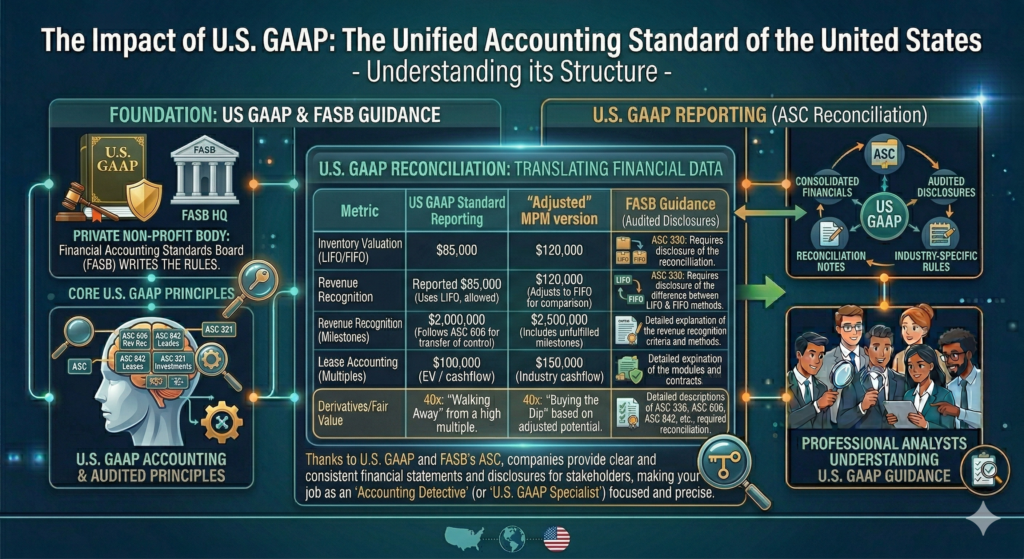

Companies often use “Non-GAAP” or “Adjusted” numbers (like adjusted EBITDA) in their press releases. Under IFRS 18, MPMs are no longer just “marketing numbers” – they are now part of the audited Financial statements.

An MPM is a subtotal of Income and Expenses that a company uses in its public communications (Outside of Financial statements like press releases or investor presentations) to explain its Financial performance.

While official IFRS numbers are the “legal truth”, MPMs are the “Management’s truth“. Professional Analysts use MPMs to understand how a CEO thinks about the Business.

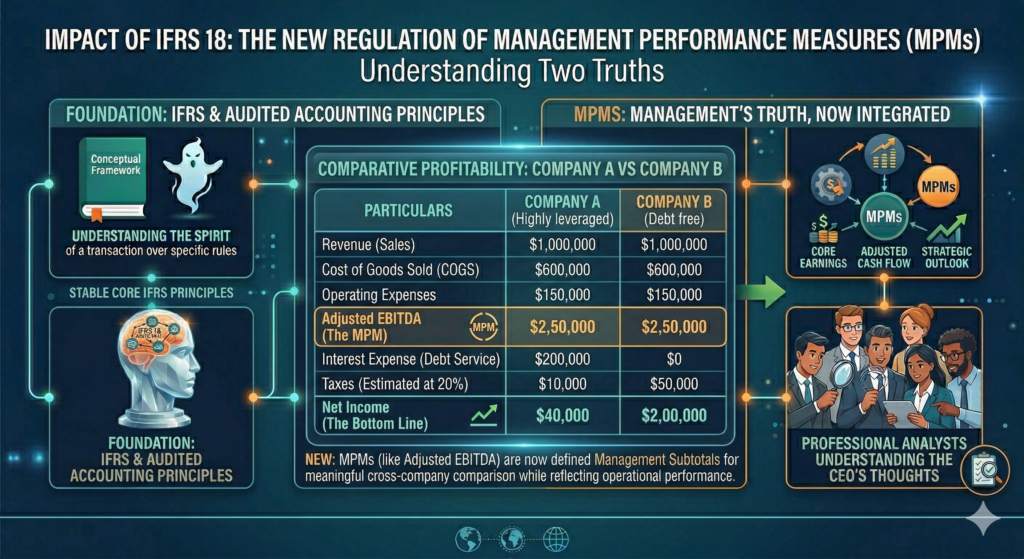

CASE STUDY 1 :- “The Tale of Two Engines”

Below is a comparison of two companies in the same Industry. Both generated $1,000,000 sales in this year.

| PARTICULARS | COMPANY A (Highly leveraged) | COMPANY B (Debt free) |

| Revenue (Sales) | $1,000,000 | $1,000,000 |

| Cost of Goods Sold (COGS) | $6,00,000 | $6,00,000 |

| Operating Expenses | $1,50,000 | $1,50,000 |

| Adjusted EBITDA (The MPM) | $2,50,000 | $2,50,000 |

| Interest Expense (Debt Service) | $2,00,000 | $0 |

| Taxes (Estimated at 20%) | $10,000 | $50,000 |

| Net Income (The Bottle Line) | $40,000 | $2,00,000 |

The Debt Trap in Company A : Company A’s Net income is $40,000. Looking only at Net Income, an ameteurr Investor might think “company A is failing”. However the MPM (Adjusted EBITDA) reveals that the Business is actually very healthy – It’s just being strangled by $200,000 in interest payments.

The Insight : Company A pays much less in taxes ($10K vs $50k). Interest expense is Tax – deductible. This is a classic level 1 corporate issuers concept. While Debt is risky, it provides a Tax shield that reduces the Government’s take.

The conclusion : If you only looked at Net Income, You’d buy company B. But if you use the MPM (Adjusted EBITDA), you realize if that company A can restructure its debt or lower its interest rates, it could be a value play with massive upside. This is why analysts add back interests to see the business without the baggage of its bank loans.

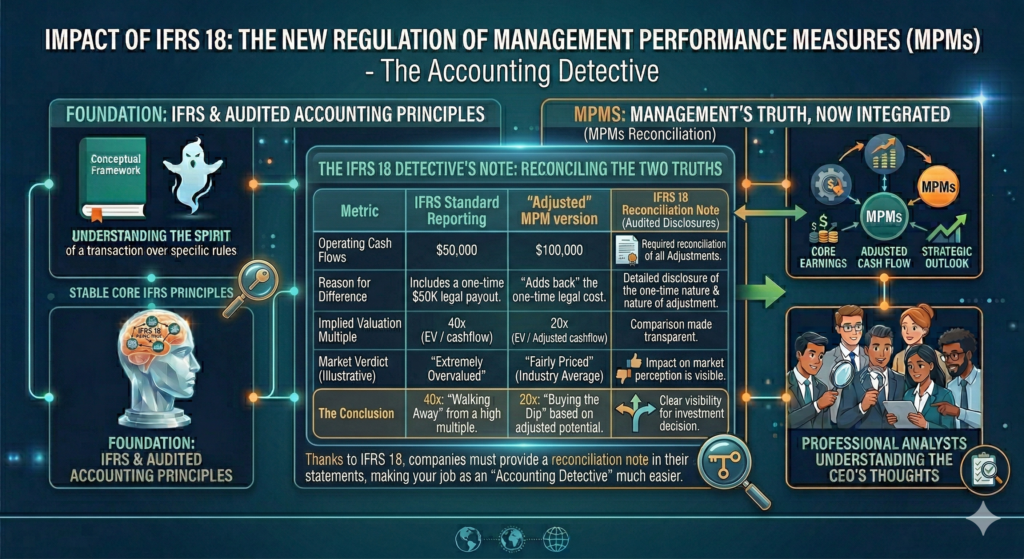

Case Study 2 : The Saas valuation Trap

In the SaaS (Software as a service) world, Net income is often negative because companies spend heavily upfront to acquire customers. Let’s take the example of CloudScale Inc., a high growth SaaS company, currently being valued by the market at an Enterprise value {EV} of $2,000,000.

| Metric | IFRS Standard Reporting | “Adjusted” MPM version |

| Operating Cash flows | $50,000 | $1,00,000 |

| Reason for Difference | Includes a one time $50K legal payout. | “Adds back” the one – time legal cost. |

| Implied valuation Multiple | 40x (EV / cashflow) | 20x (EV / Adjusted cashflow) |

| Market verdict | “Extremely overvalued” | “Fairly priced” (Industry Average) |

The Skewed Analysis (IFRS) : Under IFRS, the Cashflow statement includes everything. If cloudscale Inc., had a one-time legal settlement or a weird tax timing issue, it makes their “Cashflow from operations” look tiny. As a result, the Stock looks insanely expensive at 40x cashflow.

The clean Reality (MPM) : Professional Analysts use an MPM (Adjusted operating cashflow). By adding back that one – time 50K legal expense, we see the company’s recurring ability to generate cash is actually $1,00,000.

The conclusion : The difference between 40x and 20x is the difference between “walking away” and “buying the dip”. High growth SaaS companies are almost never valued on Net income. They are valued on Cashflow multiples. Thanks to IFRS 18, companies can no longer hide these adjustments in obscure press releases. They must provide a reconciliation note in their audited statements, making your job as an “Accounting Detective” much easier.

Final Thoughts : Why IFRS is the Bedrock of Global Finance?

IRFS are more than just a set of Accounting rules, they are the “global passport” for financial data. In a world where an investor can buy shares of a company, IFRS provides the Standardized grammar that makes that conversation possible.

U.S. GAAP (Generally Accepted Accounting Principles) is the standard framework of guidelines for financial Accounting used in the united states. In the U.S, the Financial Accounting Standards Board (FASB) is the private, non – profit body that actually write these rules.

This refers to the core engine of U.S. GAAP. While a lemonade stand might run on cash basis (counting money only when it hits the jar), global finance runs on Accruals. This system decouples Economic events from cash movements, allowing an analyst to see the true “earning power” of a company.

- The core logic – Revenue and Matching :- The powerhouse is fueled by two mandatory GAAP principles

- Revenue Recognition : Revenue is recognized when it is earned and realizable. If Boeing delivers a jet in December but doesn’t get paid until February, GAAP says that revenue belongs in the December financial statements.

- The Matching principle : We must record the expenses used to generate revenue in the same period as that revenue. Example : If a salesperson is paid a commission in January for a sale made in December, that expense must be “Accrued” back to December.

- The Powerhouse Components :- GAAP uses four specific Accounting entries to bridge the gap between cash and reality.

| CATEGORY | DEFINITION | IMPACT ON FINANCIALS |

| Accrued Revenue | You did the work; haven’t been paid. | Increases Assets (Accounts Receivable) |

| Deferred Revenue | You got the cash; haven’t done the work. | Increases Liabilities (Unearned Revenue) |

| Accrued Expenses | Use the service; haven’t paid yet. | Increases Liabilities (Accounts payable / Accrued Liabilities). |

| Prepaid Expenses | You paid early; haven’t used the service. | Increases Assets (Prepaid Assets). |

>> The Analyst’s “Red Flags” :- The “Accrual powerhouse” is where most earnings management (manipulation) happens. Analysts use Accrual Ratios to see if a company’s profits are “high quality”.

- High Accruals = Low Quality Earnings : If Net Income is consistently much higher than Cash Flow Operations (CFO), the company is likely using aggressive accruals.

- The Red Flag : If Accounts Receivable is growing much faster than Revenue, the company might be “Channel stuffing” (sending unrequested goods to distributors to inflate sales numbers).

- The Valuation Risk : Accruals eventually have to “reverse”. If a company over-accrues revenue today, they will have a massive “miss” in future quarters when the cash fails to show up.

>> The Accrual vs. Cash Flow Formula :-

Cash Flow from Operations (CFO) = Net Income + Non-cash Expenses (Depreciation)

Analyst Insight : A company can report record “Accrual Profits” while simultaneously going bankrupt because they ran out of “Actual cash”. This is why the Statement of Cash flows is the “Truth teller” in GAAP.

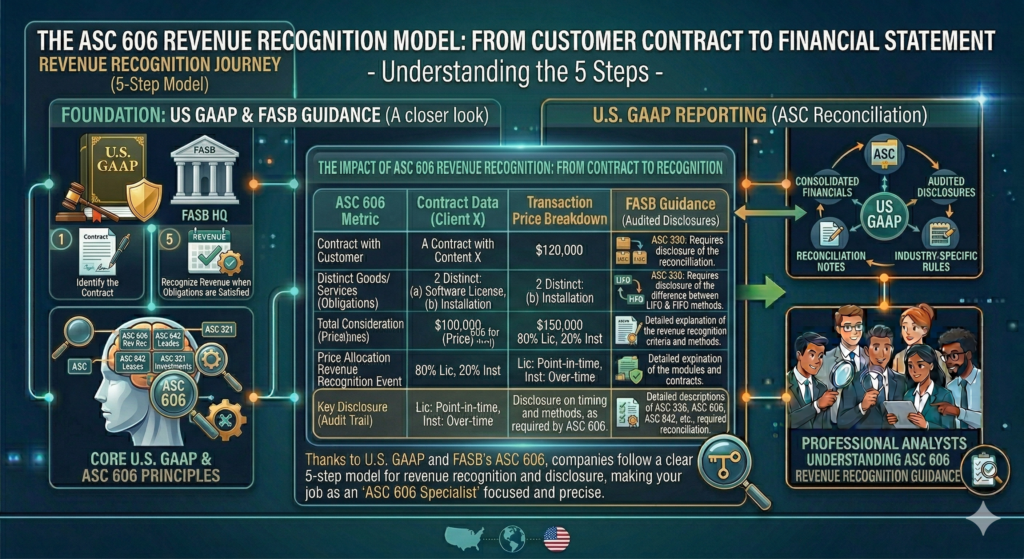

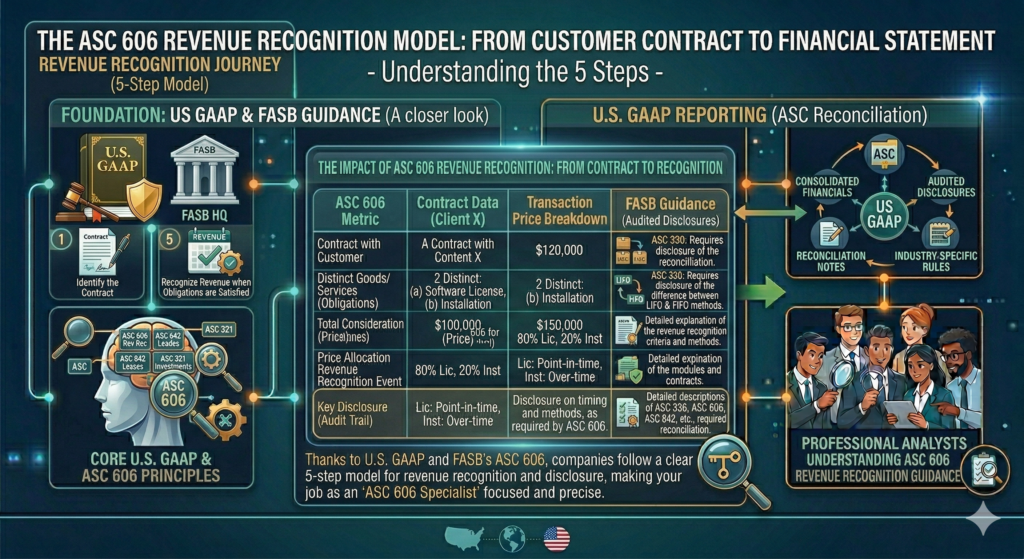

This Revenue can be recognized using the five step model :

- Identify the Contract

- Identify performance obligations

- Determine the transaction price

- Allocate the price

- Recognize Revenue when obligations are satisfied

GAAP follows the matching principle. If you sell a widget today, you must record the cost of Goods sold (COGS) today, even if you haven’t paid your supplier yet. To make ASC 600 and the Matching principle stick, let’s look at a real world example that uses this model everyday.

Apple Inc :- Imagine you walk into an Apple store and buy an IPHONE 15 bundle for $1200. This bundle includes the phone, a one year subscription to Apple TV+, and 24/7 tech support.

Part 1 : The ASC 606 Five step Model :: Apple cannot simply book the full $1200 as revenue the moment you swipe your card. These steps have to be followed.

- Identify the Contract : You agreed to buy the bundle; Apple agreed to provide the device and services.

- Identify performance obligations : there are 3 distinct promises to be made

- The Hardware (IPHONE)

- The software service (Apple TV+)

- The service obligation (Tech support).

- Determine the Transaction price : Total price is $1200.

- Allocate the price : Apple must split that 1,200 based on “Standalone selling prices”.

- I Phone : $1000

- Apple TV+ : $100

- Tech support : $100

- Recognize Revenue :

- The IPHONE(1000) : Recognized immediately because “control” transferred when you walked out the door.

- Apple TV + and support (200) :This is Deferred Revenue. Apple recognizes this over time (eg. 1/12th every month) as they provide the service.

Part 2 : Expense Recognition (The Matching Principle) :- This is the hidden side of the transaction . Even if Apple hasn’t paid its parts suppliers yet, the Matching principle kicks in.

- The Scenario : To build that IPHONE, Apple bought a screen from Samsung for $100 on credit. Apple hasn’t actually sent the cash to Samsung yet.

- The Rule : Because Apple recognized the $1000 in revenue from your purchase today, they must recognize the $100 cost of that screen as COGS (Cost Of Goods Sold) today.

- The Result (Income Statement) : Shows a Gross Profit of 900 (1,000 Rev – 100 COGS).

- Balance Sheet : Shows an “Account payable” of 100 (the debt to Samsung).

NOTE 1 :- If Apple didn’t follow the Matching Principle, they would show 1,000 in “pure profit” this month and a random 100 loss next month when they finally pay Samsung. That would make their Financial performance look like a roller coaster and mislead Investors.

NOTE 2 :- If a company is struggling to meet earnings targets, they might “Accelerate” revenue recognition by claiming they satisfied a performance obligation earlier that they actually did.

NOTE 3 : In the Apple Example, if Apple claimed the full 1,200 immediately (ignoring the service obligations), they would be “overstating” current earnings at the expense of future periods.

Conclusion :- The choice between two truths

IFRS : THE SPIRIT OF THE LAW

IFRS is a principle – based framework. It trusts management to use professional judgement to reflect the “economic substance” of a transaction. While this allows for more nuance (like Revaluation Model or capitalizing development costs), it puts the burden on the analyst to dig through the “Notes to the Financial Statements” to ensure those assumptions are realistic.

U.S. G.A.A.P : The Letter of the Law

U.S. G.A.A.P is rules-based. It provides a rigid, standardized “Instruction manual” (the ASC) to ensure that two different companies in the same industry account for things exactly the same way. While this reduces management’s ability to “massage” the numbers, It can sometimes lead to “check-the-box” accounting that misses the broader economic context.

The Bottom line for Analysts : With the Introduction of IFRS 18, the gap is closing in terms of transparency. Management Performance Measures (MPMs) are moving from “Marketing fluff” into audited reality.

Under IFRS, watch for Management discretion and aggressive revaluations and under U S GAAP, watch for rigid rules that might hide the true economic spirit of a deal.